Understanding Your Online-Offline Growth Mix is No Longer an Option for Founders

Before the pandemic, I used to point to online sales as a great, less risky alternative channel to get initial sales going. It supplemented foodservice, café, and farmer’s market sales nicely and, if DTC, it provided a market research laboratory to iterate your offering. The market research value of DTC remains, but the pandemic has enabled early-stage consumer brands to get more scale out of the channel quickly. This means you want to treat it more like a major conventional channel (e.g., mass, grocery, club).

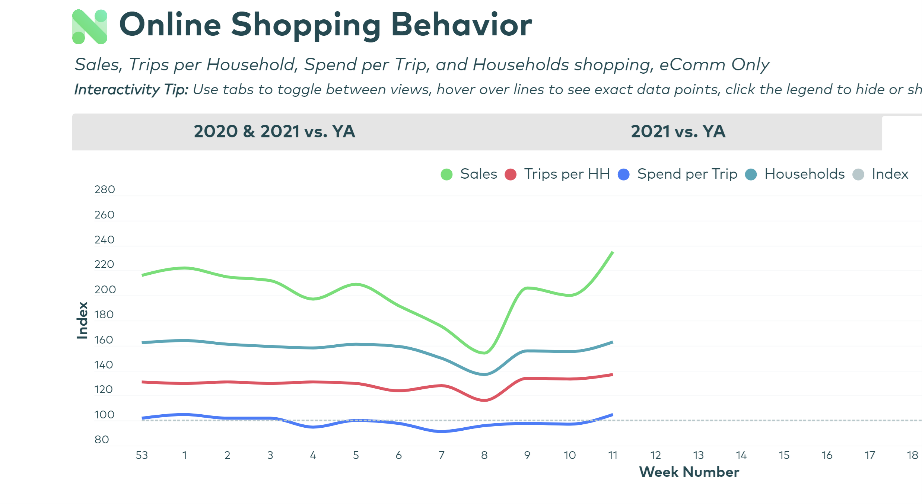

What’s happening online in Q1 (excluding DTC sales) confirms my initial thoughts on the turbo-charging of online grocery last year due to the pandemic. How? Well, we are seeing an acceleration in online $/HH vs. 2 Years Ago (i.e., pre-pandemic; see below) even as foot traffic to brick retail is growing (or returning).

I hypothesized last year that millions of sporadic online grocery buyers pre-pandemic would ratchet up their % of groceries purchased online and reach an awareness tipping point somewhere around 50% of monthly spend. This is where prior research I’ve done has indicated that online grocery becomes very habitual and sticky. The amount of time saved on in-store shopping suddenly becomes aware to the consumer at around 50% of monthly grocery spend online.

The recently elevated baseline sales rate suggests that much of the online $ share gains from the pandemic will remain permanent as COVID becomes endemic in the world. The recent boost doesn’t have a clear explanation, though, and part of me wonders if our increased mobility has reminded us what a time suck it is to shop in brick retail, causing a backlash (?).

I recently worked with a client whose category experienced a massive surge during the pandemic but whose growth appears mostly to be continuing online, not offline. In other words, the category growth in total has shifted online for now. This is more likely in my view among longer purchase cycle categories (toilet paper, soap, ketchup) that, honestly, had long ago gathered increasing amounts of monthly dust in supermarket shelves. It’s even more likely if the brand is a Skate Ramp brand with the DNA those lucky brands have.

Understanding your category’s online/offline growth mix will be important for both investors and founders moving forward in 2021. If growth is moving online or not is the first thing to look for. The YOY differences will not be as dramatic in 2021. Instead, you need to understand the new baseline growth rates in your category. For fast-growing emerging brands, like my clients’ businesses, it could radically alter how and where you spend promotional dollars for years to come.

Looking back to the client I just mentioned, they are investing in a new kind of marketing team that combines performance online marketing attacking specific online channels (e.g., Instacart, Amazon, etc.). They are also investing in more traditional brand awareness marketing activities (offline and online). For Phase 3 and Phase 4 businesses selling more than $3M annually, getting this mix right could significantly affect a brand’s ability to maintain exponential growth and do it cost-effectively.

Online is now a channel that vastly increases your ability to pay for growth acceleration scientifically. And the amount of scale you can achieve has grown in many categories in just one year, especially at the scale that early-stage businesses operate.